American Health Care: Charged the Most, Able to Pay the Least

The bill arrived without warning: over $1,000 for lab tests drawn as part of a routine physical. The patient, a Medicare beneficiary who had been seeing the same doctor for years, stared incredulously. He called his doctor’s office. The office had simply forgotten to flag him as a Medicare patient when submitting the lab order. Once they corrected the oversight and resubmitted the claim, Medicare settled it for roughly $100.

The same tests, drawn on the same day at the same lab for the same patient, cost the uninsured payer ten times what Medicare pays the lab.

This kind of story is usually filed under “billing error” and forgotten once it’s resolved. But the more useful question isn’t why the mistake happened; it’s why the gap was so large. Why does a routine blood panel cost over $1,000 when billed as an uninsured patient and $100 when billed to another payer, and what would it take for a patient to know, before the needle goes in, what any of it will cost? The answer, it turns out, is that you have to ask. Almost nobody does, and finding the answer is never easy.

The price nobody asks for

A patient can determine the price of a lab test in advance, but it takes industry knowledge. A patient who wants to know can ask their doctor’s office, which can query the lab to determine their negotiated price. Uninsured patients can ask if a special, pre-pay option is available — something most major labs offer on request. The information exists. The problem is that almost nobody requests it. The doctor says a test is needed, the patient agrees, the order goes in, and the bill arrives weeks later, by which point the test has been run, and any chance of comparison has passed. Healthcare is nearly unique among consumer expenditures in its resistance to price-shopping. Even a patient inclined to shop has nowhere to take their business, because a physician’s office generally works with a single laboratory, and the specimen goes wherever that office sends it. The system does not encourage patients to ask; it is structured to accommodate the fact that they won’t.

What the price is not

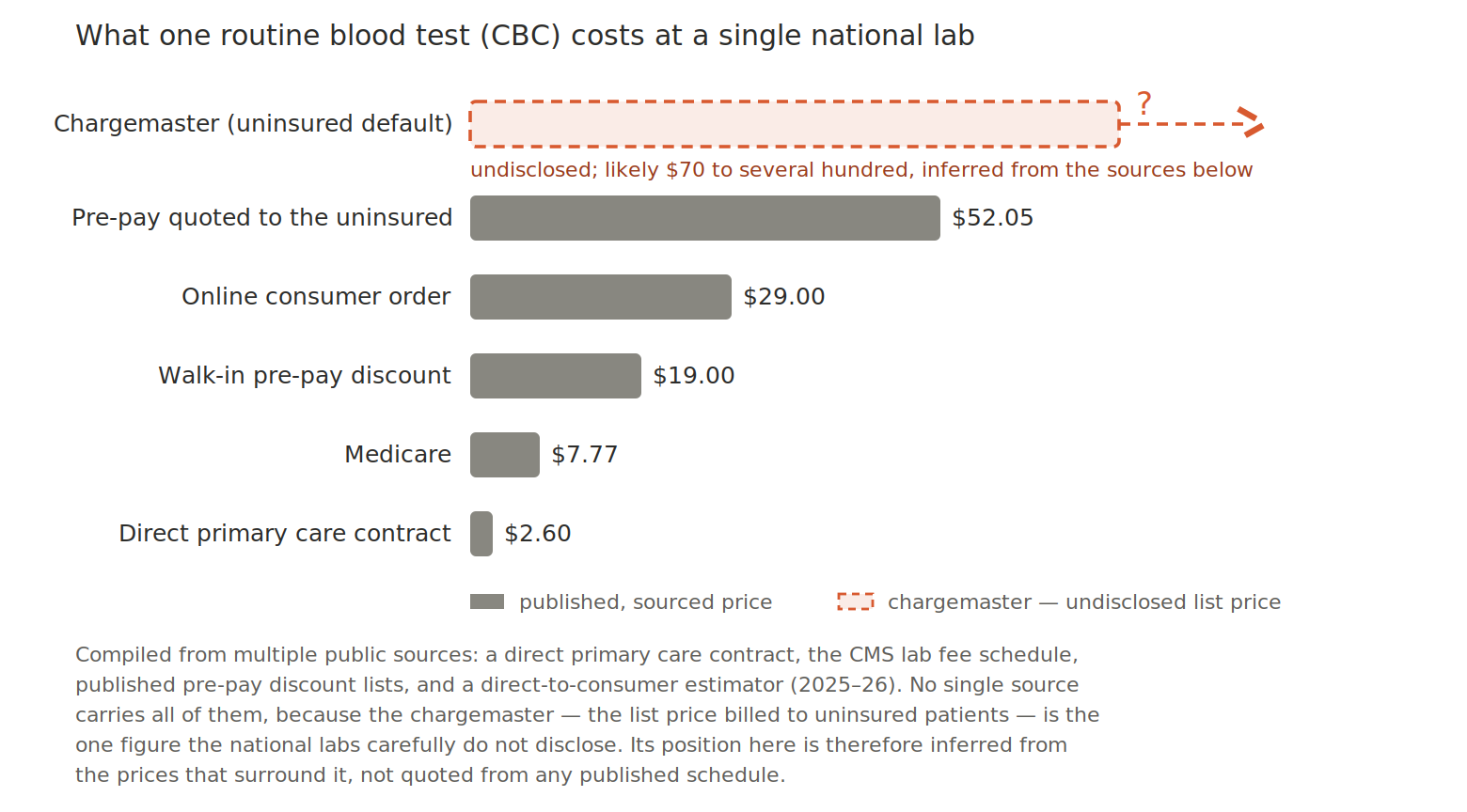

Before explaining how lab pricing works, it is worth establishing what it has nothing to do with: cost. Consider this: A direct primary care clinic that negotiates directly with a large national laboratory on behalf of its patients published its 2025 price schedule. A complete blood count: $2.60. A comprehensive metabolic panel, covering 14 separate measurements of kidney function, liver function, electrolytes, and blood glucose: $3.64. A hemoglobin A1c: $2.93. A lipid panel: $3.25.

These prices exist because the clinic sends a high volume of tests to the lab daily, and they use that volume as leverage to secure the best possible prices for their patients. Note that laboratory companies maintain commissioned field sales forces whose compensation is tied to the dollar volume they generate from physician and clinic accounts. A practice that orders a significant number of tests every day is a prized account that the sales team will negotiate hard to keep. At these prices, the lab is covering its marginal cost, the labor and materials to process one additional sample through equipment that is already running. It is not losing money; it is setting a price at the lowest point where the incremental business can cover these direct costs and provide a small margin.

Those prices could not sustain a laboratory’s full operation if applied universally, because fixed costs (analyzers, facilities, compliance, the sales force itself) have to be recovered somewhere. But they establish something important: the direct cost of running a CBC is demonstrably less than $2.60, and whatever the lab charges any other payer is not a function of cost. It is a function of what that payer will bear, and of how much leverage they have brought to the conversation.

Most patients bring none.

What the uninsured bear

An uninsured patient is typically billed at the chargemaster rate, the lab’s published list price, which can run many multiples of what Medicare pays for an identical test. A Vitamin D test that Medicare reimburses at roughly $30 has been the subject of litigation in which a patient was billed $292 for the same draw, roughly ten times the Medicare rate, by the same lab that would accept a small fraction of that figure from an insurer.

That gap was not always so wide. Each time Medicare reduced its reimbursement, the same logic was applied: the list price was raised to recover the revenue lost to regulated payers, and because the uninsured patient sits at the top of the schedule with no one negotiating on their behalf, those increases compounded against them year after year. The ten-to-one figure is the result of a formula applied over and over, not a single decision anyone set out to make. And none of these prices is posted anywhere that a patient can readily access in advance.

The transparency rules that weren’t

Regulators have not ignored the problem; they simply have not fixed it. The one serious attempt at price transparency was aimed at hospitals rather than laboratories, and even there it has largely failed. The hospital price transparency rule, in effect since January 2021, required hospitals to publish their standard charges, including negotiated insurer rates. Compliance has been poor and worsening, with barely a fifth of reviewed hospitals fully compliant and only a handful of penalties issued across thousands of reviews. And all of it applies only to hospitals. The requirements do not apply to the commercial clinical laboratories that process the overwhelming majority of routine blood work, so a patient trying to use transparency rules to understand a lab bill is, in most cases, looking in entirely the wrong place.

A bipartisan failure

Healthcare price transparency has had genuine advocates in both parties. It has also been consistently under-enforced by both. The hospital rule originated under a Republican administration and has been inadequately enforced under administrations of both parties since then. Many legislative proposals to impose meaningful requirements on laboratories have repeatedly surfaced among members of both parties and consistently failed to advance.

The explanation is not complicated. The healthcare industry, comprising hospitals, insurers, pharmaceutical companies, and laboratories, is among the most durable lobbying forces in Washington, operating across party lines because its interests span them. Real transparency would compress margins that exist precisely because prices are hidden, and patients don’t ask, and the industry has organized itself to keep both conditions in place. Organized medicine, for its part, has rarely had strong incentives to disturb an arrangement in which the patient’s bill is someone else’s problem.

What you can do, and what would actually fix it

In the near term, ask your doctor’s office or the lab for the pre-pay or cash price before non-emergency work, and understand that it is not the chargemaster rate. The chargemaster price is the inflated default billed to the uninsured; the cash price is a discount the lab will extend if asked, often dramatically lower, and at times lower even than what a high-deductible plan would apply toward your deductible. Ask for an itemized bill afterward, and if a bill seems disconnected from reality, verify that your insurance was on file when the order was placed. Errors of this kind are common, correctable, and rarely corrected without the patient’s initiative.

These are workarounds. A genuine solution would require that prices be posted in a form patients can use before a test is ordered: specific to their insurance, searchable, and up to date. The information already exists. The contracts are written, and the price schedules, including those that put a CBC at $2.60, are real and enforceable. What is missing is not information but the political will to require that any of it be made legible to the person who ultimately receives the bill. That absence is not a technical problem but a choice, made consistently and across party lines.

A note on variation: if the amount you were billed differs from the figures here, that is not necessarily an error. Prices vary by insurer, by state, by the billing pathway your physician’s office used, and by whether your insurance was correctly on file. The variation is real, largely legal, and almost entirely invisible to the people it affects most.

Sources: 2025 price schedule of a direct primary care clinic reflecting contracted pricing with a large national laboratory (on file); CMS Clinical Laboratory Fee Schedule (2025); Nolan v. Laboratory Corporation of America, M.D.N.C. No. 1:21-cv-00979 (Vitamin D billing); Patient Rights Advocate hospital transparency compliance reports (2024).